The worldwide market for Oil & Gas Materials Testing is anticipated to exhibit a compounded annual growth rate (CAGR) of 6.33% during the period spanning from 2025 to 2031. Notably, the market’s valuation in 2023 stood at USD 1230.01 million, and this valuation is poised to ascend significantly to reach USD 2000.90 million by the concluding year of the aforementioned period.

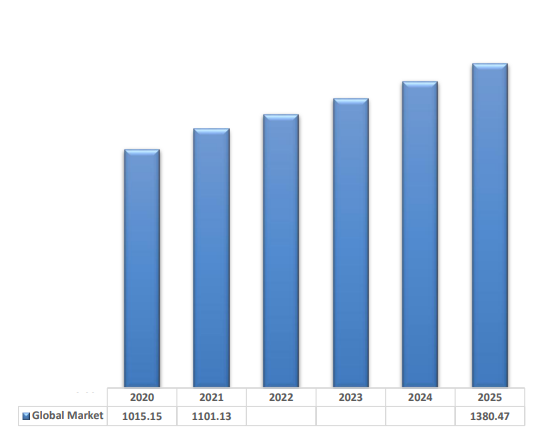

GLOBAL OIL & GAS MATERIALS TESTING MARKET SIZE, (2020-2025), (USD MILLION)

Source: Primary Research, Secondary Research, White Paper, Others Publications, Company Website

In the period spanning from 2020 to 2025, the global market size for Oil & Gas Materials Testing demonstrated a consistent upward trajectory, as illustrated in above. Commencing at $1015.15 million in 2020, the market experienced successive growth, reaching $1380.47 million by 2025.

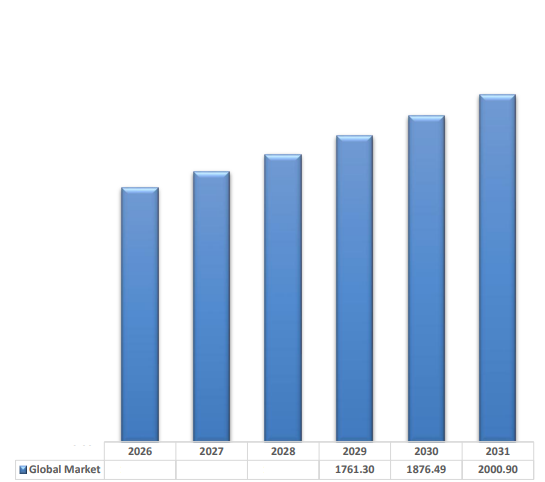

GLOBAL OIL & GAS MATERIALS TESTING MARKET SIZE, (2026-2031), (USD MILLION)

Source: Primary Research, Secondary Research, White Paper, Others Publications, Company Website

The trajectory of growth is expected to continue from 2026 to 2031, as depicted in above. Forecasts indicate a steady expansion in the global market for Oil & Gas Materials Testing, with values progressing from $1464.82 million in 2026 to an estimated $2000.90 million in 2031. This extrapolated growth signifies a Compound Annual Growth Rate (CAGR) of 6.33% during the period from 2025 to 2031.

The global market for Oil & Gas Materials Testing is a dynamic landscape, witnessing robust growth across different By Testing Type, By End User, By Testing Methods & Techniques.

By Testing Type

The Global Oil & Gas Materials Testing Market is experiencing steady growth, driven by the increasing demand for robust testing solutions to ensure the integrity and reliability of materials used in exploration, production, and transportation. The market encompasses various testing types, each serving a crucial role in maintaining safety and efficiency within the industry.

Metallurgical Testing remains a significant segment, as it plays a vital role in assessing the microstructure, hardness, and composition of metals used in oil and gas infrastructure. In 2020, the market for this testing type stood at $297.80 million, and by 2024, it is projected to reach $374.97 million. With a CAGR of 5.76% from 2025 to 2031, the segment is expected to grow consistently, driven by the industry’s focus on high-performance alloys and corrosion-resistant materials.

Mechanical Testing is another essential segment, covering tensile, impact, and fatigue testing to ensure the durability and strength of materials under extreme operational conditions. The market for mechanical testing was valued at $265.99 million in 2020, rising to $337.94 million in 2024. With a CAGR of 6.07%, it is expected to surpass $510.46 million by 2031, reflecting the growing need for enhanced mechanical properties in deepwater and high-pressure drilling environments.

Sour Service Corrosion Testing is witnessing the highest growth rate among the testing types, with a CAGR of 7.41% from 2025 to 2031. Given the challenges posed by hydrogen sulfide (H₂S) in sour gas environments, this testing method is crucial in preventing material degradation. The market size for this segment stood at $207.95 million in 2020 and is projected to exceed $458.41 million by 2031, as more oil and gas projects venture into aggressive corrosive conditions.

Coatings Performance Testing plays a key role in ensuring that protective coatings applied to pipelines, rigs, and storage tanks perform effectively against corrosion and environmental damage. This segment was valued at $105.60 million in 2020, reaching $132.20 million in 2024. With a CAGR of 5.68%, it is expected to reach $194.61 million by 2031, supported by the rising demand for advanced coating solutions in offshore and subsea applications.

Crack Tip Opening Displacement (CTOD) Testing, a specialized fracture toughness test, is gaining prominence as deepwater and high-pressure drilling activities increase. The segment was valued at $52.79 million in 2020, with projections indicating growth to $69.19 million in 2024. With a CAGR of 6.90%, it is expected to reach $110.37 million by 2031, emphasizing the industry’s focus on crack resistance and structural integrity.

Finally, Failure Analysis of Metals is crucial for identifying the root causes of component failures in critical oil and gas operations. This segment, valued at $85.02 million in 2020, is expected to reach $110.17 million by 2024 and grow to $172.24 million by 2031, with a CAGR of 6.59%. The rising incidence of material failures and the need for improved quality assurance are key growth drivers.

By Metallurgical Testing

Metallurgical testing is a fundamental aspect of the Global Oil & Gas Materials Testing Market, ensuring that materials used in pipelines, drilling equipment, and offshore structures meet stringent industry standards. The overall metallurgical testing market has grown from $297.80 million in 2020 to $374.97 million in 2024, and with a CAGR of 5.76% from 2025 to 2031, it is projected to reach $554.81 million by 2031. This growth is driven by increasing material performance requirements, regulatory compliance, and the industry’s focus on safety and durability in extreme operational environments.

Chemical Composition Analysis is one of the most critical metallurgical tests, ensuring that the elemental makeup of metals aligns with specifications to prevent failures in high-pressure and high-temperature oil and gas operations. This segment was valued at $103.80 million in 2020 and is expected to grow to $127.29 million in 2024. With a CAGR of 4.98% from 2025 to 2031, it will surpass $178.88 million by 2031, highlighting the increasing demand for precise alloy compositions in offshore and deepwater applications.

Hardness Testing evaluates a material’s resistance to deformation, which is essential for oil and gas infrastructure exposed to abrasive conditions. With an industry-wide focus on longer-lasting materials, the hardness testing segment has expanded from $75.48 million in 2020 to $93.83 million in 2024. Expected to grow at a CAGR of 5.42%, it will reach $135.78 million by 2031. This growth is largely due to the adoption of harder, more resilient metals in high-stress applications such as deep-sea drilling and hydraulic fracturing.

Microstructure Analysis plays a crucial role in detecting internal defects, grain structures, and phase compositions that can impact a component’s performance. As the oil and gas industry moves into more aggressive environments, the demand for microstructural assessments has increased. The segment was valued at $63.83 million in 2020 and is projected to reach $82.12 million in 2024. With a CAGR of 6.33% from 2025 to 2031, it is expected to exceed $126.20 million by 2031, reinforcing its importance in preventing material failures in critical infrastructure.

Mechanical Properties Testing assesses key attributes such as tensile strength, yield strength, and impact resistance, which are crucial for ensuring the structural integrity of oil and gas components. This segment has grown from $54.70 million in 2020 to $71.73 million in 2024. With the highest CAGR of 6.84% among metallurgical testing types, it is expected to reach $113.95 million by 2031. The rising adoption of advanced materials and the need to comply with evolving safety regulations are key drivers of this segment’s growth.

By Chemical Composition Analysis

Chemical Composition Analysis is a vital component of metallurgical testing in the Global Oil & Gas Materials Testing Market, ensuring that materials used in pipelines, refineries, and offshore drilling structures meet strict industry standards. With increasing regulatory requirements and the need for enhanced material performance, this segment has grown from $103.80 million in 2020 to $127.29 million in 2024. Expected to grow at a CAGR of 4.98% from 2025 to 2031, it is projected to surpass $178.88 million by 2031. The rising adoption of advanced analytical techniques to assess the chemical composition of metals and alloys is driving this growth.

Among the key methods used in chemical composition analysis, spectroscopic methods play a dominant role. These methods, including optical emission spectroscopy (OES), atomic absorption spectroscopy (AAS), and inductively coupled plasma spectroscopy (ICP), provide detailed elemental analysis to ensure compliance with industry standards. The segment was valued at $61.79 million in 2020 and is projected to reach $74.65 million in 2024. With a CAGR of 4.57% from 2025 to 2031, it is expected to exceed $102.07 million by 2031. The demand for spectroscopic methods is rising due to their precision in detecting trace elements and impurities that can impact material properties in high-pressure and corrosive environments.

Another widely used technique is X-ray fluorescence (XRF), which is essential for non-destructive material testing in oil and gas applications. XRF allows for rapid, on-site chemical analysis of metals and alloys, making it an indispensable tool in quality control and failure investigations. This segment was valued at $42.01 million in 2020 and is expected to reach $52.64 million in 2024. With a CAGR of 5.55% from 2025 to 2031, it will surpass $76.81 million by 2031. The growth of XRF technology is driven by its increasing application in pipeline integrity testing, corrosion analysis, and alloy verification, ensuring that materials meet industry standards before deployment.

By Hardness Testing

Hardness testing is a fundamental aspect of metallurgical testing in the Global Oil & Gas Materials Testing Market, ensuring that materials used in pipelines, drilling tools, and offshore platforms possess the required durability and wear resistance. The market for hardness testing has grown steadily from $75.48 million in 2020 to $93.83 million in 2024 and is expected to expand at a CAGR of 5.42% from 2025 to 2031, reaching $135.78 million by 2031. This growth is fueled by stringent material performance requirements in extreme operating environments, where hardness plays a crucial role in determining the mechanical strength of metals.

Among the various hardness testing methods, the Rockwell hardness test is one of the most widely used techniques in the oil and gas industry due to its simplicity and rapid results. This method is commonly applied to steel, alloys, and other hard metals used in high-stress components such as drill bits and casing materials. The Rockwell hardness test market was valued at $30.12 million in 2020 and is expected to grow to $36.77 million in 2024. With a CAGR of 4.87% from 2025 to 2031, it is projected to reach $51.31 million by 2031. The demand for Rockwell testing remains strong as companies increasingly focus on real-time hardness assessments to prevent material failures in harsh environments.

The Vickers hardness test, known for its precision in measuring microhardness, is particularly relevant for testing thin materials, coatings, and welds used in oil and gas applications. This test is critical for evaluating the performance of protective coatings and heat-treated alloys, ensuring their resistance to corrosion and mechanical stress. The Vickers hardness testing segment has expanded from $23.80 million in 2020 to $30.81 million in 2024 and is expected to grow at a CAGR of 6.48% from 2025 to 2031, reaching $47.82 million by 2031. The rapid adoption of automated microhardness testing in quality control processes is a key driver of this growth, helping oil and gas operators maintain the integrity of materials used in high-pressure environments.

The Brinell hardness test is another widely utilized method, particularly suited for large, coarse-grained metals such as castings and forgings used in heavy equipment and pipelines. As one of the oldest and most reliable hardness testing techniques, Brinell testing ensures that materials exposed to high mechanical loads and abrasive conditions maintain their structural integrity. This segment was valued at $21.55 million in 2020 and is projected to grow to $26.25 million in 2024. With a CAGR of 4.88% from 2025 to 2031, it is expected to reach $36.65 million by 2031. The ongoing modernization of testing equipment, including portable Brinell testers, is contributing to the steady demand for this method.

By Microstructure analysis

Microstructure analysis is a critical component of metallurgical testing in the Global Oil & Gas Materials Testing Market, enabling the examination of material properties at a microscopic level. This testing ensures the structural integrity, performance, and durability of metals used in drilling, pipelines, refineries, and offshore structures. The microstructure analysis market has grown from $63.83 million in 2020 to $82.12 million in 2024 and is projected to expand at a CAGR of 6.33% from 2025 to 2031, reaching $126.20 million by 2031. The increasing need for failure analysis, material verification, and quality control in extreme operating conditions is driving demand for microstructural evaluation methods.

Among the key techniques, optical microscopy is widely used for quick and cost-effective inspections of metal surfaces, weld joints, and coatings in the oil and gas sector. This method provides a high-level overview of grain structures, inclusions, and phase distributions, making it a fundamental tool for routine inspections and material acceptance tests. The optical microscopy market was valued at $34.89 million in 2020 and reached $44.13 million in 2024. It is expected to grow at a CAGR of 5.85% from 2025 to 2031, reaching $65.71 million by 2031. The increasing adoption of advanced digital microscopes and image analysis software is enhancing the efficiency of this technique, making it a preferred choice for oil and gas manufacturers and service providers.

On the other hand, scanning electron microscopy (SEM) provides high-resolution imaging and detailed surface morphology analysis, making it invaluable for detecting micro-cracks, corrosion patterns, and coating defects in materials exposed to high pressures and corrosive environments. The SEM market has grown from $28.93 million in 2020 to $37.99 million in 2024 and is anticipated to expand at a CAGR of 6.87% from 2025 to 2031, reaching $60.49 million by 2031. The increasing demand for advanced material characterization and failure investigation in oil rigs, refineries, and deep-sea drilling operations is a key driver for SEM adoption. Additionally, the integration of automated SEM systems with AI-powered defect recognition is further propelling market growth.

In conclusion, microstructure analysis plays a crucial role in ensuring the reliability and performance of oil and gas materials. While optical microscopy remains a cost-effective and widely used technique for initial assessments, scanning electron microscopy is increasingly adopted for detailed failure analysis and high-precision investigations. As the oil and gas industry continues to push the boundaries of material performance in extreme conditions, the demand for advanced microstructure analysis techniques will continue to rise, driving innovation and investment in this segment.

By Mechanical properties testing

Mechanical properties testing is a crucial aspect of metallurgical testing in the Global Oil & Gas Materials Testing Market, ensuring that materials used in pipelines, drilling equipment, refineries, and offshore structures meet rigorous industry standards for strength, durability, and performance under extreme conditions. The market for mechanical properties testing has seen steady growth, increasing from $54.70 million in 2020 to $71.73 million in 2024. With a projected CAGR of 6.84% from 2025 to 2031, the market is expected to reach $113.95 million by 2031. This growth is fueled by the industry’s focus on preventing equipment failures, improving safety standards, and ensuring compliance with regulatory requirements.

One of the most critical tests within this category is tensile strength evaluation, which determines a material’s ability to withstand tension without fracturing. This is particularly vital in the oil and gas sector, where high-pressure pipelines, offshore drilling components, and structural steel frameworks must endure significant mechanical stress. Over the years, tensile strength evaluation has become a key area of investment for oil and gas companies, as even minor weaknesses in materials can lead to catastrophic failures, leaks, and operational shutdowns.

Additionally, the “Others” category within mechanical properties testing includes impact testing, fatigue testing, and fracture toughness assessment, all of which are essential for evaluating long-term durability and resistance to extreme environmental conditions. As oil and gas companies push for deeper exploration and production in harsh environments such as the Arctic and ultra-deepwater fields, the need for comprehensive mechanical properties testing is set to grow further.

By Mechanical testing

Mechanical testing is a fundamental process in the Global Oil & Gas Materials Testing Market, ensuring that materials used in exploration, production, transportation, and refining operations can withstand extreme mechanical stress, pressure, and fatigue. The demand for mechanical testing has seen consistent growth, increasing from $103.32 million in 2020 to $129.81 million in 2024. With an anticipated CAGR of 5.76% to 6.62% from 2025 to 2031, the market is expected to reach $192.06 million for tensile testing, $153.84 million for impact testing, and $164.56 million for fatigue testing by 2031. This expansion is driven by the oil and gas industry’s continuous push for safer, more reliable, and high-performance materials that can operate in harsh environments, such as deep-sea drilling sites, high-pressure pipelines, and extreme temperature conditions.

Tensile testing is a critical method used to determine how materials behave under tension, ensuring that pipelines, pressure vessels, drilling equipment, and structural steel components can endure operational stresses without failure. The market for tensile testing has grown from $103.32 million in 2020 to $129.81 million in 2024, with a projected CAGR of 5.76%, reaching $192.06 million by 2031. As oil and gas operations expand into high-pressure, deep-water, and ultra-deepwater fields, tensile testing is becoming increasingly essential for evaluating new alloys, composite materials, and high-strength steel to prevent catastrophic failures.

Impact testing plays a crucial role in assessing a material’s ability to absorb sudden shocks or dynamic loads, particularly in offshore drilling structures, LNG terminals, and cryogenic storage tanks. The impact testing market has shown robust growth, increasing from $75.76 million in 2020 to $98.25 million in 2024. With a projected CAGR of 6.62%, it is expected to reach $153.84 million by 2031. The growing use of high-strength, lightweight materials in offshore and subsea applications has driven demand for impact testing, ensuring that components can withstand severe environmental conditions such as extreme cold, wave impacts, and mechanical shocks.

Fatigue testing evaluates how materials respond to cyclic stresses over time, ensuring the long-term durability and reliability of pipelines, refineries, and offshore structures that experience repeated loading and unloading cycles. The market for fatigue testing has expanded from $86.91 million in 2020 to $109.88 million in 2024, with an expected CAGR of 5.94%, reaching $164.56 million by 2031. This growth is fueled by the increasing need for high-performance materials that resist cracking, corrosion, and failure due to prolonged exposure to stress cycles in high-pressure and high-temperature environments.

By Tensile testing

Tensile testing is a crucial material evaluation process in the Global Oil & Gas Materials Testing Market, ensuring that materials used in pipelines, drilling equipment, and offshore structures can withstand high levels of mechanical stress without failure. The demand for tensile testing has been steadily increasing, growing from $103.32 million in 2020 to $129.81 million in 2024. With a projected CAGR of 5.76% from 2025 to 2031, the tensile testing market is expected to reach $192.06 million by 2031, driven by the need for stronger, more durable materials in extreme operational environments.

Stress-strain curve analysis is a key method used in tensile testing to determine how materials deform under applied stress, identifying properties such as elasticity, plasticity, and failure limits. This technique is essential for evaluating pipeline steel, pressure vessel materials, and high-strength alloys used in oil and gas operations. The market for stress-strain curve analysis has expanded from $61.42 million in 2020 to $76.02 million in 2024, with an expected CAGR of 5.34%, reaching $109.41 million by 2031. The increasing use of advanced composite materials and high-performance alloys in offshore drilling and deep-water operations has fueled demand for precise stress-strain evaluations.

Yield strength and ultimate tensile strength (UTS) measurement is a critical component of tensile testing, determining the maximum stress a material can withstand before permanent deformation or failure. This process is vital for ensuring structural integrity in high-pressure pipelines, LNG storage tanks, and deep-sea drilling platforms. The market for yield strength and UTS measurement has grown from $41.90 million in 2020 to $53.79 million in 2024, with a strong CAGR of 6.33%, expected to reach $82.65 million by 2031. The increasing demand for high-strength, lightweight materials that can withstand extreme operational conditions is driving investments in more precise and advanced testing techniques.

By Impact testing

Impact testing plays a vital role in the Global Oil & Gas Materials Testing Market, ensuring that materials used in pipelines, drilling equipment, and offshore structures can withstand sudden shocks and dynamic forces. As the oil and gas industry continues to operate in extreme environments, including deep-sea drilling and Arctic conditions, the need for impact-resistant materials has increased significantly. The impact testing market has grown from $75.76 million in 2020 to $98.25 million in 2024, with an expected CAGR of 6.62% from 2025 to 2031, reaching $153.84 million by 2031. This growth is driven by stricter safety regulations, increasing demand for high-strength alloys, and the need to reduce equipment failures in hazardous environments.

The Charpy impact test is a widely used method for evaluating a material’s toughness and ability to absorb energy upon impact. It is particularly critical for pipeline materials, pressure vessels, and offshore structures that must endure high-impact forces due to extreme weather conditions, seismic activity, or sudden mechanical stress. The market for Charpy impact testing has grown from $46.59 million in 2020 to $61.10 million in 2024, with a CAGR of 6.91% from 2025 to 2031, reaching $97.51 million by 2031. The increasing use of high-performance steels and advanced composite materials in the oil and gas industry has fueled demand for precise impact resistance assessments.

The Izod impact test is another crucial testing method, primarily used for evaluating brittle fracture resistance in various metal and polymer components. This test is essential for ensuring the durability of critical equipment, such as drilling tools, pipelines, and protective casings, which may experience repeated impact loads during operations. The market for Izod impact testing has expanded from $29.17 million in 2020 to $37.14 million in 2024, with an estimated CAGR of 6.13% from 2025 to 2031, reaching $56.33 million by 2031. The increasing adoption of polymeric and composite materials in oil and gas applications has driven the need for enhanced impact resistance testing methodologies.

By Fatigue testing

Fatigue testing is a critical process in the Global Oil & Gas Materials Testing Market, ensuring that materials used in pipelines, offshore platforms, drilling equipment, and structural components can withstand repeated mechanical stresses over extended periods. Given the harsh operating conditions in the oil and gas sector, where materials are subjected to continuous cyclic loading, pressure fluctuations, and temperature variations, fatigue testing plays a vital role in preventing catastrophic failures. The fatigue testing market has grown from $86.91 million in 2020 to $109.88 million in 2024, and it is projected to expand at a CAGR of 5.94% from 2025 to 2031, reaching $164.56 million by 2031. This growth is driven by the increasing adoption of high-strength alloys, composite materials, and stringent regulatory standards focused on safety and reliability.

Endurance limit evaluation is essential in assessing a material’s ability to withstand long-term cyclic stresses without experiencing fatigue failure. In oil and gas applications, components such as deep-sea risers, drilling strings, and subsea pipelines must endure continuous mechanical loads over years of operation. The market for endurance limit evaluation has expanded from $49.25 million in 2020 to $61.03 million in 2024, and with a CAGR of 5.38% from 2025 to 2031, it is expected to reach $88.06 million by 2031. The increasing use of corrosion-resistant materials and fatigue-resistant coatings has driven demand for precise endurance limit testing to ensure long-term structural integrity in extreme environments.

Cyclic load testing assesses a material’s ability to withstand repeated loading and unloading cycles over its service life. This is particularly critical for offshore drilling rigs, mooring systems, and high-pressure gas pipelines, where components experience constant dynamic stresses due to waves, wind, and operational loads. The market for cyclic load testing has grown from $37.67 million in 2020 to $48.85 million in 2024, and it is projected to expand at a CAGR of 6.62% from 2025 to 2031, reaching $76.50 million by 2031. The increasing focus on fatigue failure prevention and predictive maintenance has led to greater adoption of advanced cyclic load testing techniques, ensuring that materials meet industry safety standards.

By Sour service corrosion testing

Sour service corrosion testing plays a critical role in the Global Oil & Gas Materials Testing Market, ensuring that materials used in high-sulfur environments withstand corrosive conditions caused by hydrogen sulfide (H₂S), chlorides, and extreme environmental exposure. Given that oil and gas infrastructure, such as pipelines, well casings, and offshore platforms, operates in aggressive conditions, sour service corrosion testing is vital for preventing material failure, leaks, and costly shutdowns. The market for sour service corrosion testing has witnessed steady growth, driven by stringent industry regulations and increasing deepwater exploration projects. In 2024, the total market for sour service corrosion testing was valued at $278.85 million, and it is projected to grow significantly, with various testing methods expanding at a CAGR of 6.5% to 8.5% from 2025 to 2031.

Salt spray testing is a widely used method to evaluate the corrosion resistance of materials exposed to saline and humid environments, which is particularly important for offshore oil platforms and subsea pipelines. The market for salt spray testing has expanded from $64.57 million in 2020 to $88.91 million in 2024, and with a CAGR of 8.11% from 2025 to 2031, it is expected to reach $153.48 million by 2031. The rising adoption of corrosion-resistant alloys (CRAs), protective coatings, and new anti-corrosion technologies in offshore operations has fueled the demand for salt spray testing, ensuring extended service life and reduced maintenance costs.

Immersion testing is crucial for assessing material degradation in liquid environments, simulating real-world conditions where metals are continuously exposed to corrosive media such as acidic, saline, or high-temperature fluids in oil wells and pipelines. The immersion testing market has grown from $49.42 million in 2020 to $64.06 million in 2024, and at a CAGR of 6.60% from 2025 to 2031, it is projected to reach $100.23 million by 2031. The increasing drilling activities in deepwater and ultra-deepwater reserves, where materials are exposed to highly corrosive conditions, has significantly driven the demand for immersion testing.

Atmospheric exposure testing evaluates the resistance of materials to environmental factors, such as moisture, pollutants, and temperature variations, which can cause surface corrosion and long-term degradation in pipeline coatings, structural components, and above-ground storage tanks. The market for atmospheric exposure testing has grown from $40.19 million in 2020 to $51.53 million in 2024, and with a CAGR of 6.31% from 2025 to 2031, it is expected to reach $79.09 million by 2031. This growth is fueled by the increasing adoption of anti-corrosion coatings, protective paints, and high-durability materials in both onshore and offshore oilfield applications.

HIC testing is critical for detecting material susceptibility to hydrogen-related damage, which can cause unexpected pipeline failures and structural weaknesses in sour gas environments. As the oil and gas industry shifts towards high-sulfur reservoirs, the demand for HIC-resistant materials has increased. The HIC testing market has expanded from $23.37 million in 2020 to $32.53 million in 2024, and at a CAGR of 8.52% from 2025 to 2031, it is projected to reach $57.65 million by 2031. The growing use of low-carbon steels and corrosion-resistant alloys (CRAs) for sour gas applications has accelerated investment in HIC testing.

SSCC testing is essential in detecting cracking in materials exposed to H₂S-containing environments, which is a leading cause of material failure in sour service conditions. The market for SSCC testing has grown from $19.67 million in 2020 to $26.61 million in 2024, and at a CAGR of 7.75% from 2025 to 2031, it is expected to reach $44.88 million by 2031. The increasing use of high-strength alloys and specialized coatings to mitigate SSCC-related failures has driven this growth, particularly in high-pressure drilling and wellhead applications.

Full ring tests assess the integrity and performance of pipeline materials under simulated operating conditions, ensuring structural stability and crack resistance. This testing method has gained importance in verifying material compliance with industry standards. The market for full ring tests has grown from $10.73 million in 2020 to $14.21 million in 2024, and with a CAGR of 7.18% from 2025 to 2031, it is projected to reach $23.08 million by 2031. The expansion of pipeline networks and the increasing demand for non-destructive evaluation (NDE) techniques have contributed to this steady market growth.

By Phase

Salt spray testing is a critical corrosion evaluation method in the Global Oil & Gas Materials Testing Market, used to determine the durability and resistance of materials exposed to saline and humid environments. This type of testing is particularly vital for offshore oil platforms, subsea pipelines, and storage tanks, where exposure to salt-laden atmospheres accelerates material degradation. As oil and gas operations expand into harsher environments, including deepwater and ultra-deepwater reserves, the demand for reliable corrosion resistance testing continues to grow. The salt spray testing market has increased from $64.57 million in 2020 to $88.91 million in 2024, and with a CAGR of 8.11% from 2025 to 2031, it is projected to reach $153.48 million by 2031.

The ASTM B117 test is one of the most widely recognized standards for salt spray testing in the oil and gas industry. It provides controlled conditions to assess the corrosion resistance of metals, coatings, and protective finishes used in offshore rigs, marine environments, and high-salinity drilling sites. The market for ASTM B117 standard test procedures has grown significantly from $43.60 million in 2020 to $60.64 million in 2024. At a CAGR of 8.37% from 2025 to 2031, it is projected to reach $106.45 million by 2031. This growth is driven by the increased use of corrosion-resistant alloys (CRAs) and protective coatings in critical oil and gas applications. With stricter regulatory requirements mandating the use of high-durability materials, ASTM B117 testing has become an industry standard for ensuring long-term asset reliability.

Accelerated corrosion simulation is an advanced testing method designed to replicate real-world corrosive conditions faster than traditional testing techniques. This method is particularly beneficial in the development of new pipeline coatings, advanced alloys, and anti-corrosion treatments used in subsea and high-temperature oilfield environments. The market for accelerated corrosion simulation has grown from $20.97 million in 2020 to $28.27 million in 2024, and with a CAGR of 7.54% from 2025 to 2031, it is expected to reach $47.03 million by 2031. The growing emphasis on extending asset lifespan, reducing maintenance costs, and ensuring environmental compliance has fueled the demand for more rapid and precise corrosion testing techniques.

By Immersion testing

Immersion testing is a key method in the Global Oil & Gas Materials Testing Market, primarily used to evaluate material degradation in liquid environments over time. This testing plays a crucial role in assessing pipeline coatings, subsea components, and storage tanks, which are constantly exposed to harsh liquids such as crude oil, seawater, and chemical solutions. As deepwater exploration and enhanced oil recovery (EOR) techniques become more prevalent, the need for advanced immersion testing is growing. The market for immersion testing has expanded from $49.42 million in 2020 to $64.06 million in 2024, and with a CAGR of 6.60% from 2025 to 2031, it is projected to reach $100.23 million by 2031.

Long-term exposure analysis is a critical subset of immersion testing, used to assess the prolonged impact of liquid environments on metals, polymers, and composite materials. This method helps in determining corrosion rates, coating integrity, and structural weakening over extended periods. The market for long-term exposure analysis has grown from $28.74 million in 2020 to $38.17 million in 2024, and at a CAGR of 7.20% from 2025 to 2031, it is expected to reach $62.12 million by 2031. This growth is driven by rising investments in offshore drilling, floating production storage and offloading (FPSO) units, and subsea infrastructure, where prolonged exposure to corrosive liquids is inevitable.

The assessment of material degradation in liquid environments focuses on studying how different materials react when submerged in specific liquids over time. This includes analyzing chemical reactions, mechanical property changes, and potential structural failures in materials used for oil storage tanks, transportation pipelines, and processing equipment. The market for this segment has increased from $20.68 million in 2020 to $25.89 million in 2024, and with a CAGR of 5.68% from 2025 to 2031, it is projected to reach $38.11 million by 2031. The growth is primarily attributed to the increasing adoption of advanced polymers, corrosion-resistant alloys, and composite materials in oil and gas applications.

By Atmospheric exposure testing

Atmospheric exposure testing plays a vital role in the Global Oil & Gas Materials Testing Market, ensuring that materials used in pipelines, offshore structures, refineries, and storage facilities can withstand harsh environmental conditions. This testing method assesses the impact of prolonged exposure to atmospheric elements, such as UV radiation, humidity, temperature fluctuations, and pollutants, which can significantly affect the durability of materials. As the oil and gas industry expands into more extreme environments, such as deserts, offshore locations, and Arctic regions, the demand for advanced atmospheric exposure testing methods is rising. The market for atmospheric exposure testing has grown from $40.19 million in 2020 to $51.53 million in 2024, and with a CAGR of 6.31% from 2025 to 2031, it is projected to reach $79.09 million by 2031.

Natural weathering tests are essential for evaluating how materials degrade over time when exposed to real-world environmental conditions. This testing method is particularly relevant for coatings, structural metals, and polymer-based materials used in pipelines, offshore platforms, and refinery equipment. The market for natural weathering tests has increased from $22.78 million in 2020 to $28.53 million in 2024, and at a CAGR of 5.65% from 2025 to 2031, it is expected to reach $41.91 million by 2031. The steady growth of this segment is driven by the rising need for long-term durability assessments, particularly for steel, composite materials, and corrosion-resistant coatings used in oil and gas infrastructure.

Outdoor exposure simulation is a more accelerated and controlled approach to atmospheric testing, replicating severe weather conditions such as high salinity, extreme temperatures, and intense UV radiation. This method is widely used in the development and validation of protective coatings, pipeline insulation materials, and offshore equipment. The market for outdoor exposure simulation has expanded from $17.41 million in 2020 to $23.00 million in 2024, and with a CAGR of 7.10% from 2025 to 2031, it is projected to reach $37.18 million by 2031. The strong growth is attributed to the increasing deployment of oil and gas infrastructure in extreme environments, where accelerated testing is crucial to predict material performance and prevent premature failures.

By Coatings performance testing

Coatings performance testing is a critical component of the Global Oil & Gas Materials Testing Market, ensuring that protective coatings applied to pipelines, offshore structures, refineries, and storage tanks can withstand harsh environmental conditions. Protective coatings play a key role in corrosion prevention, structural integrity, and prolonging asset lifespans in the oil and gas sector. As the industry continues to expand into offshore, Arctic, and high-temperature environments, the need for advanced coatings performance testing is increasing. The overall coatings performance testing market has grown from $105.59 million in 2020 to $132.20 million in 2024, and with steady growth at a CAGR of 5.57% to 6.48% from 2025 to 2031, it is expected to reach $194.62 million by 2031.

Adhesion testing is fundamental in evaluating the bonding strength of coatings to metal substrates, ensuring long-term durability and protection against corrosion. In the oil and gas sector, coatings are applied to pipelines, storage tanks, and drilling equipment to prevent premature failures due to coating delamination or peeling. The market for adhesion testing has grown from $41.47 million in 2020 to $51.81 million in 2024, and at a CAGR of 5.57% from 2025 to 2031, it is projected to reach $75.74 million by 2031. This growth is driven by the rising adoption of advanced coatings and stricter industry standards requiring robust adhesion performance.

Impact resistance testing ensures that coatings can withstand mechanical shocks, pressure fluctuations, and sudden force applications without cracking or chipping. This is especially critical for offshore platforms, subsea pipelines, and high-pressure processing units, where mechanical stress and impact risks are high. The market for impact resistance testing has expanded from $32.26 million in 2020 to $41.62 million in 2024, and with a CAGR of 6.48% from 2025 to 2031, it is expected to reach $64.58 million by 2031. This strong growth is fueled by the increasing need for high-performance coatings that can withstand extreme operational conditions.

Cathodic disbondment testing evaluates how coatings perform when exposed to cathodic protection systems, which are commonly used in oil and gas pipelines and subsea infrastructure. This test helps determine whether coatings can maintain adhesion and integrity over long-term exposure to electrical currents. The market for cathodic disbondment tests has increased from $20.57 million in 2020 to $25.20 million in 2024, and at a CAGR of 5.11% from 2025 to 2031, it is expected to reach $35.71 million by 2031. The demand for this testing method is growing as pipeline operators and offshore facilities invest in high-performance anti-corrosion systems.

Indentation and penetration resistance testing assesses a coating’s ability to withstand mechanical penetration, abrasions, and external pressure. This is particularly important for coatings used in subsea applications, drilling risers, and high-impact areas of refineries. The market for indentation/penetration resistance testing has grown from $11.29 million in 2020 to $13.57 million in 2024, and with a CAGR of 4.60% from 2025 to 2031, it is expected to reach $18.59 million by 2031. This steady growth is due to increasing investments in advanced polymer coatings and nano-coating technologies that offer superior mechanical resistance.

By Adhesion Testing

Adhesion testing is a crucial component of the Global Oil & Gas Materials Testing Market, ensuring that protective coatings applied to pipelines, offshore platforms, storage tanks, and other critical infrastructure maintain strong adhesion under extreme operational conditions. In the oil and gas sector, coatings serve as a primary defense against corrosion, mechanical wear, and harsh environmental exposure. As the industry continues to expand into deepwater, high-pressure, and high-temperature environments, the demand for advanced adhesion testing methods is increasing. The overall adhesion testing market has grown from $41.47 million in 2020 to $51.81 million in 2024, and with a CAGR of 5.57% from 2025 to 2031, it is projected to reach $75.74 million by 2031.

The cross-hatch adhesion test is widely used in the oil and gas industry to assess the adhesion strength of coatings on metallic and composite substrates. This method involves cutting a grid pattern into the coating and applying adhesive tape to evaluate how well the coating remains intact. It is especially critical for surface coatings on offshore rigs, subsea pipelines, and storage tanks, where exposure to abrasive particles, seawater, and extreme temperatures can weaken adhesion over time. The market for cross-hatch adhesion testing has grown from $24.58 million in 2020 to $30.34 million in 2024, and with a CAGR of 5.24% from 2025 to 2031, it is expected to reach $43.39 million by 2031. This steady growth is driven by increasing investments in protective coatings, particularly nano-coatings and hybrid polymer coatings that require advanced adhesion performance validation.

The pull-off adhesion test is another critical evaluation method used to measure the tensile strength of coatings by determining the force required to detach them from the substrate. This test is especially relevant for pipeline coatings, refinery equipment, and high-stress structural components, where coating failure could lead to costly repairs, environmental hazards, and operational downtime. The market for pull-off adhesion testing has expanded from $16.89 million in 2020 to $21.47 million in 2024, and at a CAGR of 6.03% from 2025 to 2031, it is projected to reach $32.35 million by 2031. The higher growth rate of pull-off adhesion testing reflects the industry’s shift toward more stringent coating durability requirements, particularly in high-risk environments like deepwater drilling and extreme climate operations.

By Impact Resistance Testing

Impact resistance testing is a key assessment method within the Global Oil & Gas Materials Testing Market, ensuring that protective coatings and structural materials used in pipelines, drilling equipment, offshore platforms, and storage tanks can withstand mechanical shocks and sudden impact forces. In the oil and gas industry, components are frequently exposed to high-pressure conditions, abrasive environments, and mechanical stresses that can lead to material failure if coatings or structural integrity are compromised. The overall market for impact resistance testing has grown from $32.26 million in 2020 to $41.62 million in 2024, and with a CAGR of 6.48% from 2025 to 2031, it is projected to reach $64.58 million by 2031.

The evaluation of coating durability against mechanical shocks is critical in ensuring that coatings applied to oil and gas infrastructure maintain their protective properties despite harsh operating conditions. This type of testing assesses how well coatings can resist chipping, cracking, and delamination when subjected to sudden mechanical shocks, such as impacts from tools, falling debris, or high-pressure fluid surges. The market for evaluating coating durability against mechanical shocks has increased from $22.78 million in 2020 to $29.15 million in 2024, and at a CAGR of 6.24% from 2025 to 2031, it is expected to reach $44.54 million by 2031. This growth is driven by rising investments in advanced coatings, including hybrid polymer coatings and nano-ceramic coatings, which offer superior impact and abrasion resistance. Additionally, increasing safety and regulatory standards for offshore and onshore operations have made impact resistance testing a mandatory requirement for coating validation.

The assessment of resilience under impact stress is essential in determining how well materials and coatings used in critical oil and gas infrastructure can withstand repeated impacts without structural failure. This test is particularly important for pipelines, storage tanks, drill pipes, and wellhead equipment, which are regularly subjected to vibrations, heavy loads, and sudden force applications. The market for impact stress resilience assessment has expanded from $9.48 million in 2020 to $12.47 million in 2024, and with a CAGR of 7.01% from 2025 to 2031, it is forecasted to reach $20.04 million by 2031. The higher growth rate for this segment reflects the industry’s increasing focus on extending asset lifespans by using high-strength composite materials and innovative impact-resistant coatings. Additionally, as offshore drilling and deepwater exploration projects become more common, the need for materials that can endure harsh marine environments and dynamic mechanical forces continues to rise.

By Failure Analysis of Metals

Failure analysis of metals is a critical aspect of the Global Oil & Gas Materials Testing Market, ensuring the reliability and safety of pipelines, drilling equipment, pressure vessels, and offshore structures. The extreme operating conditions in the oil and gas industry, such as high pressure, temperature fluctuations, corrosive environments, and mechanical stresses, make failure analysis essential for preventing catastrophic failures, minimizing downtime, and improving material performance. The market for failure analysis of metals has grown significantly, reaching $110.17 million in 2024, and is projected to expand at a CAGR of 6.64% to reach $172.24 million by 2031. This growth is primarily driven by the increasing complexity of oil and gas infrastructure, the need for advanced material testing, and stricter regulatory compliance requirements.

Metallurgical failure analysis is a fundamental technique for identifying material defects that lead to fractures, cracks, and premature failures in oil and gas infrastructure. This includes fractography, grain boundary studies, and inclusion analysis, which help determine the root causes of material degradation due to manufacturing defects, operational stresses, or environmental exposure. The market for metallurgical failure analysis has grown from $32.21 million in 2020 to $41.88 million in 2024, and with a CAGR of 6.64%, it is expected to reach $65.70 million by 2031. The rising demand for high-strength alloys, corrosion-resistant materials, and advanced coatings in deepwater and high-pressure applications is fueling this segment’s growth.

Fatigue and stress rupture analysis is crucial for predicting component lifespan and failure modes in oil and gas systems. This analysis examines how materials degrade under repeated mechanical stress, thermal cycling, and prolonged loading conditions, which are common in drilling rigs, pipelines, and refineries. The market for fatigue and stress rupture analysis has expanded from $21.50 million in 2020 to $27.41 million in 2024, and with a CAGR of 6.16% from 2025 to 2031, it is expected to reach $41.65 million by 2031. As the industry moves toward longer operational lifespans for assets and cost-effective maintenance strategies, this segment will continue to be in high demand.

Hydrogen embrittlement and brittle fracture studies are critical for preventing sudden and catastrophic failures in oil and gas equipment. These failures occur due to hydrogen absorption, leading to cracks and brittle fracture in high-strength steels and alloys. This type of failure is particularly concerning in pipelines transporting hydrogen-rich fluids, deep-sea drilling equipment, and refineries. The market for hydrogen embrittlement and brittle fracture studies has expanded from $13.74 million in 2020 to $18.44 million in 2024, and with a CAGR of 7.53%, it is projected to reach $30.65 million by 2031. The growth of this segment is attributed to increased hydrogen production and transportation projects, stricter safety regulations, and advances in hydrogen-resistant materials.

Welding is a critical process in oil and gas infrastructure, and weld failure analysis helps identify defects, stress concentrations, and improper welding techniques that lead to failures in pipelines, pressure vessels, and offshore structures. Residual stress effects also play a significant role in weld durability and fatigue resistance. The market for weld failure analysis has grown from $9.67 million in 2020 to $12.11 million in 2024, and with a CAGR of 5.67%, it is expected to reach $17.81 million by 2031. Increasing demand for automated welding inspection techniques, such as phased array ultrasonic testing (PAUT) and X-ray computed tomography (XCT), is driving growth in this segment.

Ductile fracture and fatigue failures, along with corrosion-related failures, are among the most common failure modes in the oil and gas industry. This type of analysis is essential for detecting early-stage defects, predicting failure points, and developing corrosion-resistant alloys and coatings. The market for ductile fracture, fatigue failures, and corrosion-related failure analysis has grown from $7.90 million in 2020 to $10.33 million in 2024, and with a CAGR of 6.85%, it is projected to reach $16.43 million by 2031. The increasing adoption of predictive maintenance strategies, real-time corrosion monitoring systems, and AI-based failure prediction models is propelling this segment forward.

By End User

The Global Oil & Gas Materials Testing Market is driven by the increasing demand for high-performance materials, quality assurance, and failure prevention across upstream, midstream, and downstream sectors. As exploration and production move into harsher environments, ensuring material integrity becomes critical. The market has witnessed steady growth, reaching $1,302.33 million in 2024, with a projected CAGR of 6.28% from 2025 to 2031.

The upstream sector—which includes exploration and production (E&P) activities—is the largest contributor to the materials testing market. The harsh operating environments in deepwater, ultra-deepwater, and high-pressure, high-temperature (HPHT) reservoirs necessitate extensive material testing to ensure pipeline durability, drilling rig reliability, and well integrity. The upstream oil & gas materials testing market grew from $495.66 million in 2020 to $646.20 million in 2024, and with a CAGR of 6.73%, it is expected to reach $1,019.49 million by 2031. This growth is fueled by expanding offshore drilling activities, increasing shale gas exploration, and stricter safety regulations. Companies are focusing on advanced non-destructive testing (NDT) techniques, real-time monitoring solutions, and corrosion-resistant materials to enhance operational efficiency and minimize failures.

The midstream sector, which involves transportation, storage, and distribution of oil and gas, relies heavily on pipeline integrity management and material durability. Given the risks associated with pipeline corrosion, mechanical stress, and environmental exposure, stringent materials testing is essential to prevent leaks and ruptures. The midstream oil & gas materials testing market expanded from $333.69 million in 2020 to $425.99 million in 2024, and with a CAGR of 6.20%, it is projected to reach $648.90 million by 2031. The increasing adoption of advanced coatings, inline inspection technologies (ILI), ultrasonic testing (UT), and smart monitoring systems is driving the segment’s growth. Additionally, the rising demand for liquefied natural gas (LNG) infrastructure and cross-border pipeline projects will further boost materials testing requirements in this sector.

The downstream sector, which includes refining, petrochemical production, and distribution, requires materials testing to ensure equipment longevity, operational efficiency, and compliance with environmental regulations. The presence of high temperatures, corrosive chemicals, and mechanical wear makes material integrity testing crucial for safe and efficient operations. The downstream oil & gas materials testing market increased from $185.80 million in 2020 to $230.14 million in 2024, and with a CAGR of 5.40%, it is anticipated to reach $332.51 million by 2031. Growth in this segment is driven by expanding refining capacities, increasing demand for specialty chemicals, and stricter emissions control regulations. The sector is witnessing a surge in the adoption of advanced metallurgical analysis, fatigue testing, and thermal degradation studies to enhance asset lifespan and reduce downtime.

By Testing Methods & Techniques

The Global Oil & Gas Materials Testing Market relies on a range of testing methods and techniques to ensure material durability, structural integrity, and regulatory compliance. Given the extreme conditions faced in exploration, production, transportation, and refining, testing methods such as non-destructive testing (NDT), destructive testing, chemical analysis, failure analysis, and coating & surface testing play a vital role in preventing failures and ensuring operational efficiency. The market for testing techniques reached $1,302.34 million in 2024 and is projected to grow at a steady pace, driven by increasing investments in quality control, failure prevention, and safety regulations.

NDT is the most widely used testing method in the oil & gas sector due to its ability to evaluate material properties and detect flaws without damaging the components. The market for NDT in materials testing grew from $382.24 million in 2020 to $482.78 million in 2024, and with a CAGR of 5.86%, it is expected to reach $719.28 million by 2031. This growth is fueled by increasing pipeline inspection requirements, offshore infrastructure assessments, and advancements in ultrasonic and radiographic testing. Technologies such as phased array ultrasonic testing (PAUT), guided wave testing (GWT), and remote visual inspection (RVI) are gaining traction, especially in pipeline integrity management and structural health monitoring.

While NDT is essential for real-time monitoring, destructive testing remains crucial for detailed material analysis, particularly in stress, fatigue, and failure resistance studies. The destructive testing segment grew from $312.51 million in 2020 to $412.61 million in 2024, and with a CAGR of 7.09%, it is projected to reach $666.63 million by 2031. This segment is experiencing significant demand from upstream drilling operations, refining equipment analysis, and pipeline burst testing. Common techniques include tensile testing, impact testing, fracture mechanics testing, and creep testing, which are widely applied to evaluate material durability, pressure resistance, and mechanical performance under harsh operating conditions.

Chemical analysis plays a key role in corrosion control, alloy composition testing, and contaminant detection. The segment has grown from $156.55 million in 2020 to $196.76 million in 2024, and with a CAGR of 5.78%, it is expected to reach $291.66 million by 2031. With increasing concerns regarding sulfide stress cracking, hydrogen embrittlement, and material degradation in harsh environments, the demand for spectroscopic analysis, chromatography, and X-ray fluorescence (XRF) techniques has increased significantly. Additionally, chemical compatibility testing of materials used in LNG storage tanks, refineries, and offshore platforms is becoming a key area of investment.

Failure analysis is crucial for investigating material breakdowns, root cause identification, and prevention of future failures in oil & gas operations. The failure analysis market expanded from $110.14 million in 2020 to $143.63 million in 2024, and with a CAGR of 6.76%, it is projected to reach $227.10 million by 2031. This segment is highly relevant to pipeline failures, wellbore integrity assessments, and refinery equipment breakdowns. Methods such as fractography, microstructural analysis, and stress rupture testing are being widely adopted to enhance safety and minimize costly downtime.

Corrosion is one of the biggest challenges in the oil & gas industry, making coating and surface testing a critical requirement. This segment grew from $53.71 million in 2020 to $66.56 million in 2024, and with a CAGR of 5.41%, it is anticipated to reach $96.23 million by 2031. Testing methods such as salt spray testing, adhesion testing, and wear resistance evaluation are being used to ensure pipeline coatings, offshore platform protection, and refinery surface durability. With growing investments in anti-corrosion coatings and nanocoating technologies, this segment is expected to witness steady demand.

Driver, Restraint, Challenge and Opportunities Analysis

Market Driver

Increasing Focus on Asset Integrity and Safety Regulations:

The oil and gas industry operates in high-risk environments where infrastructure failures can result in catastrophic accidents, financial losses, and environmental disasters. Governments and regulatory bodies worldwide have implemented strict safety and quality standards, such as API (American Petroleum Institute), ASTM (American Society for Testing and Materials), ASME (American Society of Mechanical Engineers), and NACE (National Association of Corrosion Engineers), to ensure materials used in pipelines, refineries, and offshore platforms meet rigorous performance requirements. These regulations mandate periodic testing, quality assurance, and failure analysis of materials, thereby driving demand for specialized oil and gas materials testing services. Compliance with these regulations helps mitigate operational risks, extend asset life, and maintain workforce safety.

As exploration and production activities move into harsh and extreme environments, such as deepwater drilling and Arctic operations, the need for high-strength, corrosion-resistant materials has increased. Advanced testing methods, including Non-Destructive Testing (NDT), fatigue testing, and corrosion resistance evaluation, are now essential to verify material performance under high pressure, extreme temperatures, and corrosive conditions. The enforcement of zero-tolerance policies on equipment failure by regulatory bodies further strengthens the demand for continuous monitoring, condition assessment, and failure analysis services, fueling growth in the oil and gas materials testing market.

Aging Infrastructure and Rising Maintenance Needs:

A significant portion of the global oil and gas infrastructure, including pipelines, offshore platforms, and refineries, has been in operation for several decades, leading to concerns about material degradation, corrosion, and fatigue failures. Many pipelines and facilities built in the 1960s and 1970s are still in use today, requiring extensive material testing to ensure continued operational integrity. Aging infrastructure is particularly susceptible to stress corrosion cracking, hydrogen embrittlement, and fatigue-related failures, making periodic Non-Destructive and Destructive Testing (DT) a necessity. As companies aim to extend the life of their assets, they increasingly rely on materials testing to identify vulnerabilities before they lead to catastrophic failures.

Additionally, midstream and downstream operators are investing in advanced coatings, composite materials, and corrosion-resistant alloys to protect infrastructure from environmental and operational stresses. Cathodic protection testing, coating adhesion tests, and failure analysis of corroded structures play a crucial role in these efforts. With aging assets requiring more frequent and intensive testing, service providers offering comprehensive testing solutions are experiencing increased demand, positioning the oil and gas materials testing market for steady growth.

Expansion of Oil & Gas Exploration in Extreme Environments:

The depletion of conventional oil and gas reserves has pushed companies to explore unconventional and hard-to-reach reservoirs, such as deepwater, ultra-deepwater, and Arctic regions. These extreme environments expose materials to high pressures, low temperatures, aggressive chemical exposure, and mechanical stresses, necessitating the use of high-performance materials that undergo rigorous testing. For example, high-strength, corrosion-resistant alloys (CRAs), polymer coatings, and composite materials require extensive qualification and validation to withstand such harsh conditions.

Furthermore, the shift toward enhanced oil recovery (EOR) and high-pressure, high-temperature (HPHT) drilling techniques has introduced new challenges in material selection and durability testing. Materials must endure extreme thermal cycling, sour gas exposure (H2S), and abrasive wear, requiring specialized mechanical, thermal, and chemical testing. The growing exploration of shale gas and tight oil formations using hydraulic fracturing techniques has also created demand for fracture toughness analysis, fatigue testing, and failure analysis of drilling equipment, well casings, and fracking fluid-resistant materials.

Technological Advancements in Testing Methods:

The advancement of material testing technologies has revolutionized the oil and gas industry by enabling more accurate, efficient, and real-time assessment of material performance. Innovations in NonDestructive Testing (NDT), such as digital radiography, phased array ultrasonic testing (PAUT), eddy current array testing (ECAT), and acoustic emission monitoring, have improved the ability to detect subsurface defects, stress corrosion cracking, and fatigue-related damage without disrupting operations. These advanced NDT methods reduce inspection downtime, operational costs, and safety risks, making them increasingly preferred by oil and gas operators.

Additionally, developments in computer-aided failure analysis, 3D imaging, and machine learning-based predictive maintenance have enhanced the ability to analyze material failures and predict potential weaknesses before they cause significant damage. The integration of Internet of Things (IoT) sensors in materials testing allows for continuous condition monitoring of pipelines and refinery equipment, providing real-time data on material degradation, corrosion rates, and structural integrity. These advancements have significantly improved decision-making, asset performance management, and maintenance planning, driving increased adoption of sophisticated materials testing solutions.

Growth in Midstream and Downstream Infrastructure Investments:

The expansion of liquefied natural gas (LNG) terminals, petrochemical refineries, and pipeline networks has increased demand for materials testing services to ensure structural integrity, corrosion resistance, and mechanical performance. The rapid growth of LNG production and transport, driven by rising global energy demand and the transition toward cleaner fuels, requires materials that can withstand cryogenic temperatures, high pressures, and dynamic loading conditions. Testing methods such as cryogenic impact testing, fatigue analysis, and fracture mechanics evaluation are essential for validating materials used in LNG storage tanks, gas pipelines, and pressure vessels.

Similarly, the expansion of petrochemical and refining capacity in regions like the Middle East, AsiaPacific, and North America has led to increased demand for chemical analysis, high-temperature corrosion testing, and coatings performance evaluation. Refineries process high-sulfur crude oil, which can lead to accelerated corrosion and material degradation, requiring stringent testing to ensure compliance with industry standards such as API 571 (Damage Mechanisms in Refining Industry) and NACE MR0175 (Sour Service Materials Testing). As investments in midstream and downstream infrastructure continue, the need for comprehensive material testing solutions will grow, sustaining market expansion.

Market Restraint

High Costs Associated with Advanced Testing Techniques:

The adoption of highly sophisticated testing techniques, such as phased array ultrasonic testing (PAUT), acoustic emission monitoring, computed radiography (CR), and fracture mechanics analysis, requires significant investment in specialized equipment, skilled personnel, and laboratory infrastructure. Many oil and gas companies, especially small and medium-sized enterprises (SMEs), struggle to allocate substantial capital for in-house testing facilities. The high cost of acquiring, maintaining, and calibrating advanced testing instruments discourages widespread adoption, particularly in cost-sensitive markets.

Furthermore, third-party testing services can also be expensive, making it challenging for companies operating on tight profit margins to afford regular material assessments. Deepwater and ultra-deepwater projects, which require more frequent and stringent materials testing, often face even higher testing expenses due to the complexity of equipment and logistics. As a result, cost concerns act as a significant barrier, particularly in regions where oil and gas exploration budgets are limited or where companies prioritize operational cost-cutting measures over proactive maintenance and testing.

Volatility in Oil & Gas Prices Impacting Capital Expenditure:

The oil and gas industry is highly cyclical and price-sensitive, with market fluctuations directly influencing capital investments in exploration, production, and infrastructure maintenance. When crude oil prices decline, companies often reduce spending on non-essential activities, including material testing, quality control, and equipment assessments. Historically, downturns in oil prices (such as those in 2014-2016 and during the COVID-19 pandemic in 2020) resulted in delays and cancellations of infrastructure projects, leading to a decline in demand for materials testing services.

Additionally, uncertainty in energy markets due to geopolitical tensions, supply chain disruptions, and economic downturns further limits investment in advanced testing technologies. Companies tend to defer or minimize testing procedures to maintain profitability during low oil price periods, impacting overall market growth. The long-term sustainability of the oil and gas materials testing market remains highly dependent on stable oil prices and continuous investment in asset integrity programs.

Market Opportunity

Rising Demand for Advanced Non-Destructive Testing (NDT) Techniques

The growing emphasis on asset integrity management and predictive maintenance in the oil and gas industry is driving demand for advanced Non-Destructive Testing (NDT) techniques. Methods such as phased array ultrasonic testing (PAUT), guided wave testing (GWT), acoustic emission testing (AET), and digital radiography (DR) allow for real-time monitoring of pipelines, storage tanks, offshore structures, and drilling equipment without causing damage to components. As companies seek to reduce downtime and prevent catastrophic failures, investments in automated and AI-driven NDT solutions are increasing.

Furthermore, the integration of robotics and drones for remote NDT inspections in hazardous environments presents a lucrative opportunity. Autonomous robotic crawlers equipped with ultrasonic and eddy current sensors are being increasingly deployed in offshore platforms and subsea pipelines to conduct thorough inspections while minimizing human intervention. This trend is expected to expand the market for high-tech materials testing services as oil and gas companies continue adopting digitized and remote testing technologies to enhance operational efficiency and safety.

Expansion of Oil & Gas Infrastructure Projects in Emerging Markets:

The rapid growth of oil and gas exploration, refining, and pipeline infrastructure projects in emerging economies such as India, China, Brazil, and the Middle East presents significant opportunities for the materials testing market. As these countries expand their upstream, midstream, and downstream operations, there is an increasing need for strict material quality assessments, corrosion resistance testing, and failure analysis to ensure long-term durability and regulatory compliance.

Additionally, the expansion of liquefied natural gas (LNG) terminals, petrochemical plants, and refinery upgrades in response to rising global energy demands creates a surge in demand for coatings performance testing, fracture mechanics evaluations, and metallurgical failure analysis. Governments in these regions are enforcing stricter safety and quality standards, driving further adoption of specialized material testing services to ensure pipeline integrity, structural stability, and corrosion prevention.

Increasing Focus on Corrosion and Coating Testing Solutions:

Corrosion remains one of the biggest challenges in the oil and gas sector, leading to substantial economic losses due to pipeline leaks, structural degradation, and equipment failures. As companies shift towards longer operational lifespans for assets, there is a growing emphasis on coating performance testing, cathodic protection verification, and high-temperature corrosion resistance assessments. Materials testing providers have the opportunity to expand their offerings in specialized corrosion-resistant coatings, thermal spray coatings, and polymeric protective layers that can extend the lifespan of oil and gas infrastructure.

Furthermore, advancements in nano-coatings and self-healing protective layers are opening new avenues for coating and surface testing solutions. The integration of smart coatings with embedded sensors to provide real-time corrosion monitoring and predictive analytics is a game-changer. As companies seek innovative ways to reduce maintenance costs and unplanned shutdowns, coating and surface testing services are expected to experience strong demand growth in the coming years.

Adoption of Digital Twin Technology for Materials Testing:

The oil and gas sector is increasingly leveraging Digital Twin technology to simulate material behavior under real-world conditions and predict structural weaknesses before failure occurs. Digital twins allow for virtual simulations of pipelines, drilling rigs, and refineries, enabling companies to analyze material fatigue, stress distribution, and corrosion progression in real-time. This opens significant opportunities for predictive materials testing solutions that integrate artificial intelligence (AI), machine learning, and big data analytics.

Moreover, the implementation of cloud-based testing platforms allows companies to centralize materials testing data from multiple locations, improving decision-making and failure prevention strategies. AIpowered automated defect recognition (ADR) is also gaining traction, enabling faster and more accurate detection of material inconsistencies. As oil and gas firms continue their digital transformation journeys, material testing service providers offering integrated digital solutions will benefit from long-term growth prospects.

Market Challenges

Increasing Regulatory Complexity and Compliance Burden:

The oil and gas industry is subject to stringent regulatory requirements governing materials testing, asset integrity management, and environmental safety. Regulatory bodies such as API, ASTM, ASME, NACE, and ISO impose strict guidelines on pipeline materials, refinery components, and offshore structures, requiring rigorous testing and certification before assets can be deployed. However, the constantly evolving regulatory landscape creates compliance challenges for oil and gas companies, particularly for those operating in multiple regions with different testing requirements.

Additionally, failure to comply with industry standards and government regulations can result in heavy penalties, legal liabilities, and reputational damage. Keeping up with the latest material testing standards, documentation procedures, and certification renewals requires continuous investment in compliance management systems and third-party auditing services. For many companies, the complexity of navigating regional and global regulatory frameworks adds to the overall operational burden, making materials testing a time-consuming and resource-intensive process.

Challenges in Testing New Materials for Extreme Operating Conditions:

The oil and gas industry is increasingly adopting next-generation materials such as high-performance alloys, composite materials, and advanced coatings to enhance the durability of pipelines, drilling equipment, and offshore structures. However, testing these new materials under extreme conditions— such as high-pressure subsea environments, corrosive refinery processes, and hydrogen transportation systems—remains a major challenge. Traditional testing methods may not be fully effective in evaluating the long-term performance of these innovative materials, requiring the development of customized testing protocols and advanced simulation techniques.

Additionally, material degradation in high-temperature, high-pressure (HTHP) environments poses unique challenges that are difficult to replicate in laboratory settings. Ensuring that new materials meet industry performance benchmarks requires extensive failure analysis, fatigue testing, and corrosion resistance evaluations, which can be costly and time-consuming. Companies must invest in advanced testing methodologies such as digital twin simulations and AI-driven predictive modeling, but integrating these technologies into existing workflows is often a slow and complex process.

Recent Developments,

The Global Oil & Gas Materials Testing Market plays a critical role in ensuring the reliability, durability, and safety of materials used in upstream, midstream, and downstream operations. The industry is driven by the need to mitigate risks associated with corrosion, mechanical stress, extreme temperatures, and chemical exposure in harsh operational environments. As the oil and gas sector evolves, stringent regulatory frameworks and quality control standards continue to push companies toward advanced nondestructive testing (NDT), destructive testing, failure analysis, and coatings performance evaluations to ensure operational efficiency and compliance with safety regulations.

Post-COVID-19, the market has experienced a gradual recovery, with increased investments in infrastructure, pipeline integrity management, and offshore exploration projects driving demand for specialized testing services. The emergence of digital and automated testing solutions, such as AI-driven inspections and remote monitoring techniques, has further revolutionized material testing processes. However, the industry also faces significant challenges, including volatile oil prices, supply chain disruptions, and the rising adoption of alternative energy sources, which are reshaping long-term market dynamics.

Opportunities exist in the development of high-performance materials, hydrogen-compatible infrastructure testing, and advanced coatings technologies to extend the life of critical assets. Additionally, the integration of IoT and real-time monitoring systems in materials testing is expected to enhance predictive maintenance capabilities, reducing unplanned downtime and improving asset longevity. Companies that invest in sustainability-driven testing methodologies and multi-industry diversification will be well-positioned for long-term growth, particularly as global energy transitions gain momentum.

Despite growth prospects, the market faces challenges such as increasing costs of specialized testing equipment, a skilled labor shortage, and stringent environmental regulations that require continuous adaptation. However, innovation in automated testing solutions, robotics-assisted inspections, and hybrid testing methodologies is expected to mitigate these challenges, ensuring continued market expansion. As the oil and gas industry transitions toward enhanced safety, efficiency, and sustainability, the demand for comprehensive materials testing solutions will remain robust, shaping the future of the global market.

Market Breakup By Testing Type

Metallurgical Testing

Mechanical Testing

Sour Service Corrosion Testing

Coatings Performance Testing

CTOD Testing

Failure Analysis of Metals

Market Breakup By Metallurgical Testing

Chemical Composition Analysis

Hardness Testing

Microstructure Analysis

Mechanical Properties Testing

Market Breakup By Chemical Composition Analysis

Spectroscopic methods

X-ray fluorescence (XRF)

Market Breakup By Hardness Testing

Rockwell hardness test

Vickers hardness test

Brinell hardness test

Market Breakup By Microstructure Analysis

Optical microscopy

Scanning electron microscopy (SEM)

Market Breakup By Mechanical Properties Testing

Tensile strength evaluation

Others

Market Breakup By Mechanical Testing

Tensile Testing

Impact Testing

Fatigue Testing

Market Breakup By Tensile Testing

Stress-strain curve analysis

Yield strength and ultimate tensile strength measurement

Market Breakup By Impact Testing

Charpy impact test

Izod impact test